Most fintech startups aim for the broadest possible audience. CRED started by telling 97% of users they weren’t eligible.

It focused on the elite 3% of credit card holders in India: those with the highest credit scores. By 2026, that narrow focus paid off: CRED captures 22% of the country’s credit card payment volume, up from 6 million users in 2021.

In India’s $51.30 billion fintech market, CRED carved out a niche by focusing on trust over scale. The numbers are striking: ₹2,473 crore revenue in FY2024, 66% revenue growth, and a 41% reduction in losses by 2026.

So, how can a company built on exclusivity and trust become one of India’s fastest-growing fintech unicorns? This article breaks down the cred business model, operating model, and revenue model to answer that question.

What is CRED?

The cred business model centers on a fintech startup that provides users with a platform to pay their credit dues, rent and other bills, all in one place while earning additional rewards for doing so on time. It provides users with an instant credit line and enables a safe space for P2P lending between high trust individuals at interest rates which are way more beneficial than the traditional lending sources.

The Idea Behind CRED Business Model

A brainchild of Kunal Shah, CRED was launched in April 2018, with the idea of capitalising on the industry of high trust individuals who would be rewarded for their responsible financial behaviour.

The idea behind the cred business model is to create a gated ecosystem of high trust credible individuals and eventually build ways for them to link and connect with one another. It is a credit-based ecosystem that provides a safe space for individual lenders and financial institutions to lend money to trustworthy individuals.

It uses the creditworthiness of individuals in the form of their credit scores as a measure to filter the community. Then to retain customers, it rewards them in the form of CRED coins if they make timely payments through the platform.

Who Are CRED’s Customers?

CRED targets to garner a significant share of wealthy, affluent, and trustworthy customers who own and use credit cards. The cred business model creates a gated community of loyal and credible individuals to eventually build mechanisms for them to connect and expand on many other possibilities in the future.

CRED’s Value Proposition

Famous for its excellent user experience, the cred business model stands out by providing the following value to its customers:

- The cred app is an all in one application for paying credit dues, rent and other bills in just five taps. It reduces the hassle of handling multiple credit cards by making the process tremendously simplified, easy and convenient.

- It provides users with an instant credit line and facilitates P2P lending at an interest rate of 9% to lenders, which is way more than what savings accounts and deposits usually offer.

- It records loan caps, analyses hidden costs and overall expenses of the users and tracks due dates and sends them timely reminders to make payments.

- If users make timely payments, it rewards them with CRED coins which they can redeem on the platform ‘Discover’ to avail discounts on different products offered by CRED partners.

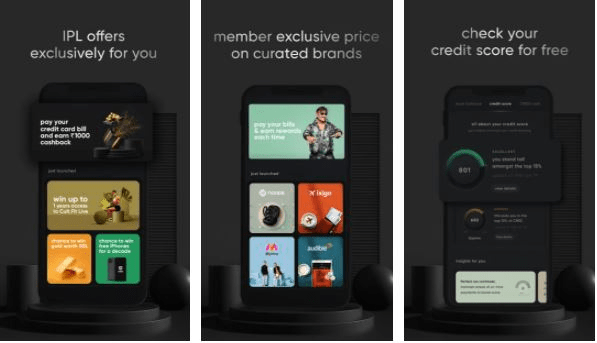

- Users can also calculate their credit scores for free and use CRED’s help to maintain a good credit profile and make good financial decisions.

Most importantly, CRED is a niche community of high-trust creditworthy individuals. It works along the lines of the velvet rope effect, where people ‘pay together and can play together’. This creates a social network with a tremendous scope of connecting people with a realm of other possibilities!

How Does CRED Operate?

Once the user downloads the cred app and enters their mobile number, the app checks the cards connected to the registered phone number till the account gets configured. If the credit score is greater than 750, the person is allowed to use the app. If not, he is sent to the waiting list. After receiving access, CRED apps will have access to the mail identification for reading and scanning credit card receipts like due dates and service statements.

Key Activities

The key activities that the cred business model provides its users are CREDIT management, CRED Stash, CRED Mint, RentPay, CRED Store and CRED travel.

CREDIT Payments

CRED provides a unified payments interface to the users and enables them to pay their credit card and other bills through the app and receive rewards in the form of CRED coins if they do so on time. They can then use these vouchers and discounts to avail offers on products of companies CRED has tie-ups with. It analyses user expenses and sends reminders for timely payments.

CRED Stash

CRED Stash is an instant credit line offered by CRED to provide its customers credit with greater ease at an interest rate equivalent to about one-third of the usual charges of using a credit card. It has a credit limit of Rs 5,00,000. It eliminates the tedious verification and application processes typically associated with loans and makes the process smooth and convenient for the users. It has partnered with various banks, like the IDFC bank for providing these loans to the customers.

RentPay

CRED’s RentPay feature allows users to pay their recurring household expenses and rent payments through the app. It gives users reminders to pay the bills timely, and making payments through the app eventually leads to rewards which they can avail on the purchase of other products.

CRED Mint

CRED launched its peer to peer lending product, CRED mint, in partnership with Liquiloans, an RBI registered P2P non-banking financial corporation(NBFC). It enables its users to lend their money and earn interest rates of up to 9 percent per annum, which is way higher than savings accounts and other traditional forms of deposits. Lenders can invest between ₹1,00,000 and ₹10,00,000, and earn returns for the period invested.

The investments made in CRED Mint are to be lent out through CRED Cash, a lending product for high trust individuals and over Rs 2415 crore have been disbursed through regulated partners.

CRED Store

CRED has partnered with various companies in multiple domains of health, travel, e-commerce and so on to allow users to spend the CRED coins they earn and avail offers and discounts while purchasing these products and services through the platform. It has partnered with over 2000 brands that offer CRED exclusive prices to the customers that they can easily access through the CRED store. This also helps those companies enhance their visibility and boost their sales through their presence on the app.

CRED Travel

CRED lets its users purchase flight tickets, book hotels, and manage their culinary expenses through the app and get rewarded with CRED coins that they can use to purchase different other products from the CRED store.

Key Channels

CRED has a website and an app as key channels through which people can make use of the platform.

Key Partners

- CRED has partnerships and tie-ups with over 2000 brands that offer their products on the platform at exclusive prices to CRED customers.

- It has tie-ups with more than 34 banks. For instance, its product CRED Stash provides its users cheap credit in partnership with the IDFC bank. Moreover, P2P lending has been facilitated through collaboration with Liquiloans; an RBI registered NBFC. It facilitates payments through the Axis Bank and participates in UPI through the Payments Service Provider(PSP) bank since it has a tripartite agreement with the sponsor PSP(Axis Bank) and NPCI, that is, the National Payments Corporation of India.

Key Resources

Beyond its partnerships, CRED’s growth relies on three core resources: its people, technology, and capital.

- Human Resources: CRED’s team has grown from about 1,600 employees in December 2022 to 2,280 by June 2026, supporting the company’s expanding product suite and operational needs. Source

- Technological Resources: The platform is built on a modern technology stack, using cloud infrastructure, real-time monitoring, and AI-driven analytics to ensure performance and security at scale.

- Financial Resources: CRED has raised over $1 billion across multiple rounds from investors like Sequoia Capital, DST Global, General Catalyst, Coatue Management, Ribbit Capital, and Insight Partners. A recent angel round of $1.99M in March 2026 reflects ongoing investor confidence. Source

CRED Market Valuation and Funding

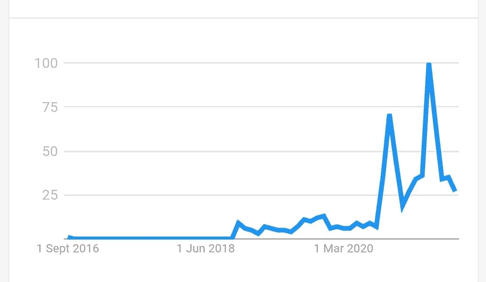

CRED’s valuation tells a story that’s common in Indian fintech right now. The company hit $6.4 billion during its 2022 Series F round. By 2026, that number had settled at $3.64 billion: a 43% decline from its peak.

The most recent round raised $72 million, led by Singapore’s sovereign wealth fund GIC through Lathe Investment. RTP Global, Sofina Ventures, and QED Innovation Labs, Kunal Shah’s family office, also joined.

Across 12+ rounds, CRED has now raised over $944 million in total. The valuation reset reflects a broader shift in Indian fintech: investors are no longer chasing sky-high multiples. Instead, they’re pushing companies like CRED toward profitability and public market readiness.

That said, the drop doesn’t signal trouble. GIC still committed fresh capital, and the company is actively expanding its product suite across lending, payments, and commerce. The valuation correction is more about market reality catching up with peak-era optimism.

CRED Revenue Model

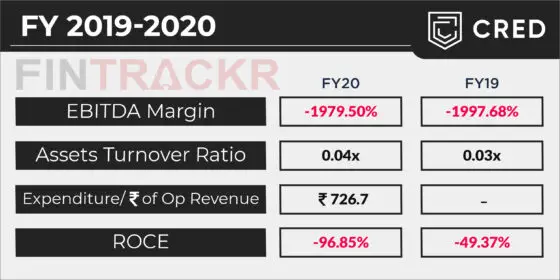

CRED’s financials tell a story of rapid growth and strategic patience. The platform reported revenue of ₹2,473 crore in FY2024, about $300 million, marking a 66% jump year-over-year. What’s more, operational losses shrank by 41%, signaling that the company is moving toward sustainability without sacrificing growth.

The cred business model monetizes only about one-third of its monthly transacting users. That leaves more than 8 million highly engaged members who haven’t yet been tapped for revenue. For context, CRED is free to use. The team chose scale over revenue in the early years, focusing on building a loyal, affluent user base first.

Sources Of Revenue For CRED

Affiliate Income

CRED earns commissions by connecting its members with financial products: credit cards, personal loans, and insurance. When a user applies for a product through the platform, CRED gets a cut. This model works because the cred app already knows its users’ financial behavior, making recommendations feel personal rather than pushy.

Revenue From Advertisements

Brands pay CRED to reach its high-income audience. The platform runs targeted ads, sponsored content, and brand collaborations within the app. Unlike typical ad models, CRED’s ads often feel like curated experiences: think exclusive product drops or limited-time offers that match the user’s lifestyle.

Transaction Fees

Every time a user pays a credit card bill or makes a payment through CRED, the platform may charge a small fee to the biller or payment gateway. It’s a volume game. Small per-transaction margins add up when you’re processing billions in payments each month.

Revenue From Loans

CRED also offers direct lending through its own products or partner banks. The app provides personal loans and credit lines to eligible members. Interest income from these loans forms a growing part of the revenue pie, especially as more users trust the platform with their financial needs.

Costs Incurred

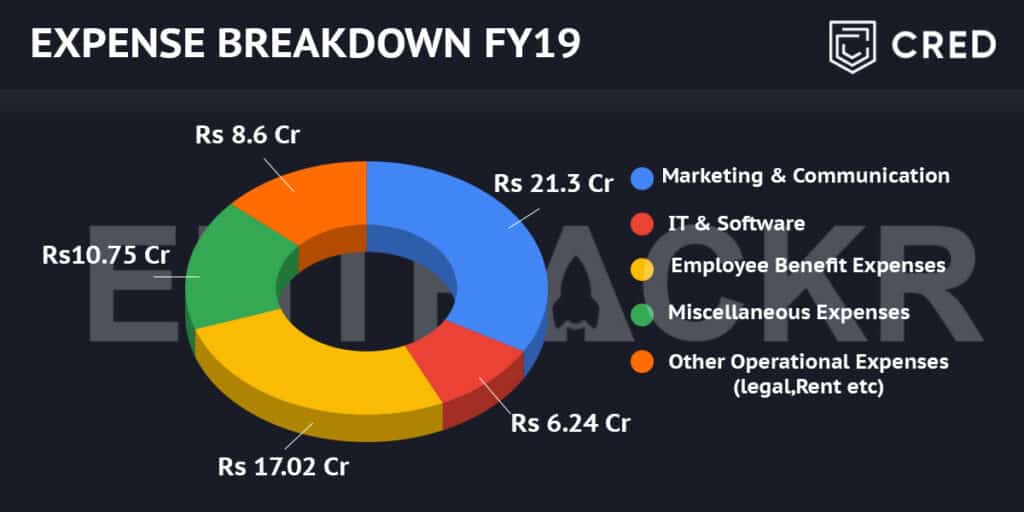

Growth isn’t cheap. CRED spends heavily on customer acquisition, technology development, and marketing. But here’s the shift: the company cut marketing expenses by 36% and reduced customer acquisition costs by 40% in FY2024. The focus is on organic growth through referrals and product stickiness, rather than expensive ad campaigns.

Research and development also eats up a significant chunk of capital. CRED is building products like UPI payments, CRED Garage for vehicle management, and other features that keep users engaged. The goal is to create multiple revenue streams while keeping the core experience free.

The result? A 41% reduction in operational losses, down to ₹609 crore in FY2024. That’s a clear sign that CRED is balancing growth with fiscal discipline: proving that you can build a large, loyal user base without burning through cash indefinitely.

Bottom-Line?

CRED has a very innovative and creative way to market itself. It delivers cakes to its users’ offices so that other people get to know about it and create a buzz effect. This helps the company initiate a viral loop, generate more customers, and create a ‘brag-worthy proposition’.

As customers continue to pay their bills and use the platform, the company will have a lot of their financial data, which they can monetise in the future. Even if they don’t sell it to some other financial institution or bank for privacy reasons, they can use the data to enhance and personalise users’ experience of the app.

It emphasises building a gated community and implementing the cred business model before expanding it further and becoming profit-oriented. Another important takeaway is that founder Kunal Shah focuses more on how the demand for services or products should determine the idea behind a startup and have a unique and brag-worthy proposition.

Go On, Tell Us What You Think!

Did we miss something? Come on! Tell us what you think of this article on CRED business model in the comments section.